The Payment

Experts

Providing our customers with

the best solutions to achieve

their evolving payment goals.

B2 Payment Solutions Inc.

At B2, we offer an extensive suite of products and services that enable us to lead our customers into the next generation of smart and secure payment solutions. By applying our services together with world-class technologies from our strategic partners, B2 delivers innovative solutions globally to our customers and partners.

B2 offers a comprehensive suite of testing products for payment transaction processing, ensuring quality, before going live.

Customized payment software development solutions that go above and beyond your expectations

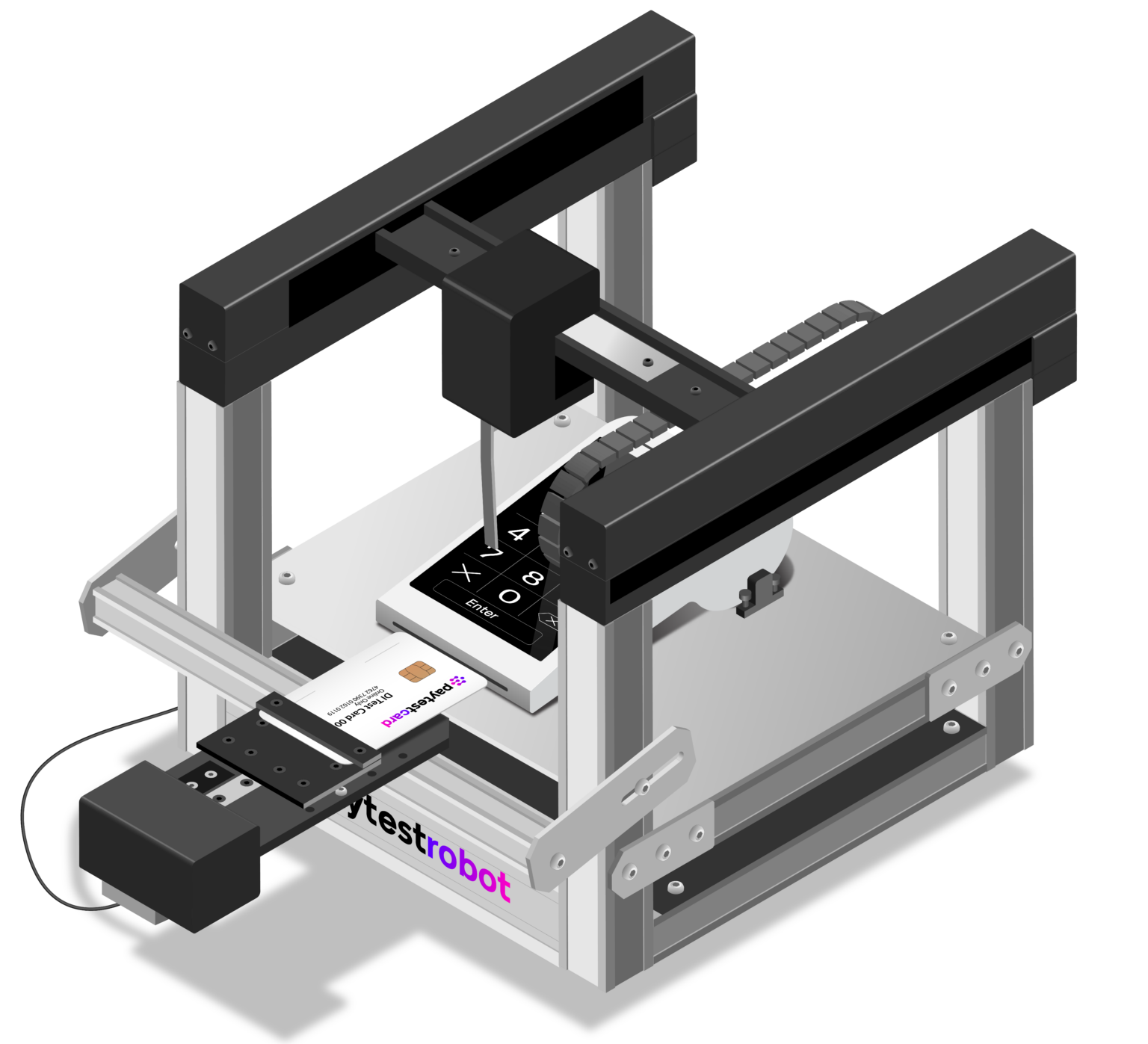

Offering a full suite of onsite or remote automated payment testing tools and services. We help organizations ensure reliability and performance of their payment test transactions.

Conduct fast, cost-effective, and high-quality payment software testing with our solution, automating up to 80% of regression or certification tests effortlessly.

Conduct fast, cost-effective, and high-quality payment software testing with our solution, automating up to 80% of regression or certification tests effortlessly.

Learn from the experts. In-person and virtual instructor-led training and eLearning courses, catering to all levels of experience within the payments industry.